Andy Pupuis

Andy PupuisIf you’ve spent any time scrolling headlines lately, you’ve probably seen the words “plunge,” “stall,” or “housing slowdown.” The truth, however, is far less dramatic — and far more interesting.

The housing market isn’t crashing. It’s normalizing.

Rates are settling, demand is steadying, and prices — while no longer racing ahead — continue to show measured growth. The national data from Freddie Mac, the National Association of Realtors (NAR), and Fannie Mae show a market that’s cooling from record heat, not collapsing into recession.

Let’s unpack what’s actually happening, what the numbers tell us, and how both buyers and sellers can make smart moves in a market that’s far more balanced than the headlines suggest.

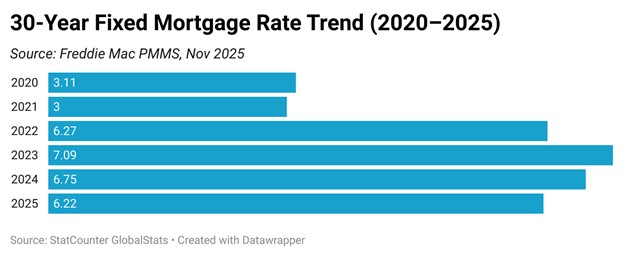

Mortgage Rates: Elevated, but Easing

Rates are the biggest driver of buyer psychology, and they’ve shifted meaningfully over the last quarter.

Takeaway:

Affordability remains a hurdle, but recent easing has already reopened doors for many buyers who paused earlier in the year. Each full percentage-point change in mortgage rates shifts buying power by roughly 10 % — enough to put many households back in the game.

Sales and Inventory: Slow but Steady

Housing transactions slowed from the pandemic highs, but they remain well within healthy historical ranges.

Interpretation:

Sales volumes are rising modestly, not declining. Inventory is improving, but still short of pre-2019 levels (around 2 million). Together, those numbers paint a picture of re-balancing, not recession.

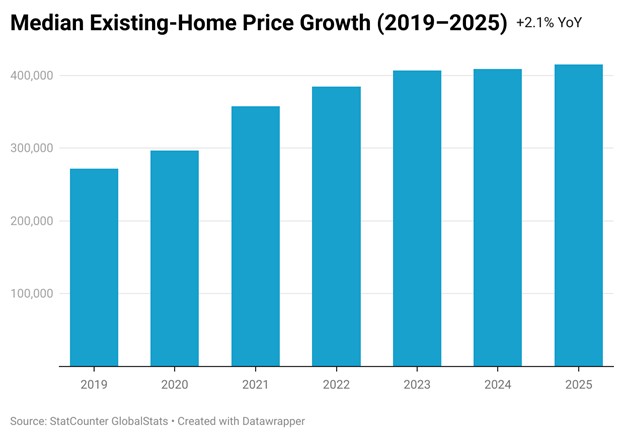

Price Stability and Home Equity

Prices are often where the myths swirl most, so let’s ground this in fact:

Interpretation:

Owners are sitting on record equity with minimal financial distress. Even if prices plateau, widespread negative equity is unlikely. That’s one of the clearest distinctions between today’s market and the pre-crash era of 2007–08.

Supply Shortage Remains Structural

Even as inventory grows, housing demand still exceeds supply:

Result:

Any “excess supply” narrative is unfounded. Builders are producing below demand, and new-home completions will take several years to catch up. This under-building continues to support home values even as transaction volume cools.

Local Angle: Western DuPage Snapshot

While national averages dominate headlines, our local markets tell a more encouraging story.

(Based on Midwest Real Estate Data / NAR Midwest Region, Oct 2025)

Translation:

Homes are taking a bit longer to sell, but pricing power remains intact. Buyers have more breathing room, and sellers still enjoy solid demand for well-presented, accurately priced properties.

Myths vs. Facts — 2025 Edition

|

Myth |

Fact |

|

“Home prices are crashing.” |

National prices rose 2.1 % YoY (NAR). 77 % of metro markets posted gains in Q3 2025. |

|

“Nobody’s buying.” |

Existing-home sales up 1.5 % MoM, new-home sales up 8 %. |

|

“The Fed’s rate cut will instantly slash mortgage rates.” |

Mortgage rates are influenced by 10-year Treasury yields — not directly by Fed funds. Expect gradual, not instant, relief. |

|

“We’re heading for a 2008-style foreclosure wave.” |

Delinquencies under 3 %, and homeowners hold record equity. |

|

“More listings mean prices will tumble.” |

Months of supply = 4.6 — a balanced level. Prices typically flatten, not fall, under these conditions. |

Economic Context

These figures confirm what the market feels: cooling inflation, steady job growth, and rising confidence. When consumers feel secure in income, housing tends to follow.

Strategic Guidance

For Buyers

For Sellers

Time strategically. Early-winter listings face less competition and attract serious buyers chasing year-end moves.

What to Watch Next

Housing is not collapsing — it’s resetting.

We’ve moved from record-low rates and bidding wars to a more sustainable, balanced environment.

For buyers, that means opportunity with less competition.

For sellers, it means pricing and presentation matter again.

Either way, those who act based on data, not drama, will navigate the next six months with confidence.