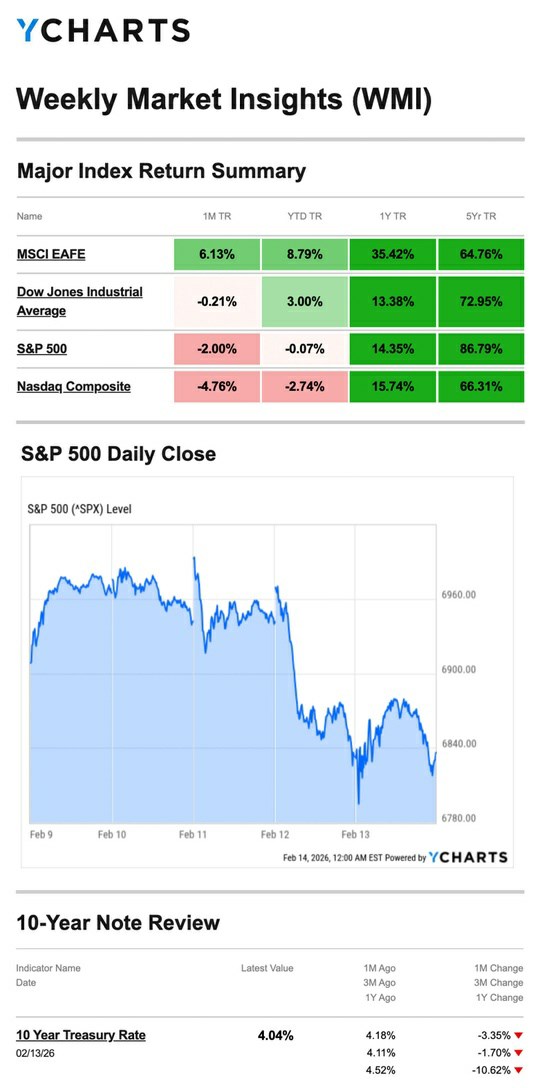

| Stocks fell last week as investors reacted to mixed economic data and concerns over signs of broadening AI disruption of business models. The Standard & Poor’s 500 Index fell 1.39 percent, while the Nasdaq Composite Index declined 2.10 percent. The Dow Jones Industrial Average slid 1.23 percent. The MSCI EAFE Index, which tracks developed overseas stock markets, rose 1.92 percent. AI Disruption Fears Big tech started last week back in the driver’s seat, leading the Nasdaq and S&P 500 to modest gains as investors appeared cautiously optimistic about the economy and Q4 corporate reports. Stocks slid modestly on Tuesday after December retail sales were flat, sparking some anxiety about the economy. Investors also fretted about the impact of artificial intelligence (AI) on financial stocks. A stronger-than-expected jobs report initially sparked a rally midweek, but momentum quickly faded as investors dug deeper into the numbers. Stocks then came under pressure as AI disruption fears spread across several industry groups. Traders worried that AI would disrupt certain business models and possibly increase unemployment. TMarkets rebounded following Friday’s Consumer Price Index (CPI) reading, which gave investors another economic data point to cheer as the pace of inflation slowed in January. |

|

|

| Source: YCharts.com, February 14, 2026. Weekly performance is measured from Monday, February 9, to Friday, February 13. TR = total return for the index, which includes any dividends as well as any other cash distributions during the period. Treasury note yield is expressed in basis points. |

Good News, Bad News Investors focused on three key economic reports out last week: retail sales, jobs, and inflation. Here are the key good news/bad news takeaways from each report: Retail sales: Consumer spending was flat in December, below expectations and below November’s 0.6 percent growth. Good news: Given that two-thirds of the economy runs on consumer spending, the Fed may reconsider its wait-and-see stance on raising rates. Employment: January job growth was mostly concentrated in a single sector. Plus, downward revisions showed employers only added 181,000 jobs last year—70 percent fewer than initially thought. There was essentially no job growth in the back half of 2025. Good news: January job growth was more than double what economists expected—the biggest gain in over a year. The unemployment rate also edged down. Inflation: Inflation was cooler-than-expected but remains above the Fed’s target. Good news: The CPI’s 2.4 percent year-over-year growth in January marked a drop from December’s 2.7 percent annual pace. |

This Week: Key Economic Data Monday: Markets closed for Presidents’ Day Tuesday: Empire State Manufacturing Survey Wednesday: Housing Starts (Nov., Dec.). Building Permits (Nov., Dec.). Durable Goods (Dec.). Trade Balance in Goods (Dec.). Retail Inventories (Dec.). Wholesale Inventories (Dec.). Federal Open Market Committee Meeting Notes (Jan.). Thursday: Weekly Jobless Claims. Trade Deficit (Dec.). Pending Home Sales. Minneapolis Fed President Neel Kashkari speaks. Friday: Gross Domestic Product (GDP), Q4. Personal Consumption Expenditures (PCE) Index (Dec.). New Home Sales (Nov., Dec.). Consumer Sentiment. * indicates publication of a report delayed by the government shutdown in October and November. Source: Investors Business Daily - Econoday economic calendar: February 13, 2026. The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to provide accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts are also subject to revision. |

This Week: Companies Reporting Earnings Tuesday: Medtronic (MDT), Palo Alto Networks, Inc. (PANW), Constellation Energy Corporation (CEG), Cadence Design Systems, Inc. (CDNS) Wednesday: Analog Devices, Inc. (ADI), Booking Holdings Inc. (BKNG), Carvana Co. (CVNA), DoorDash, Inc. (DASH), Moody’s Corporation (MCO) Thursday: Walmart Inc. (WMT), Deere & Company (DE), Newmont Corporation (NEM), The Southern Company (SO) Source: Zacks, February 13, 2026. Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your goals, time horizon, and risk tolerance. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule their earnings reports without notice. |

|

Be On Alert for IRS Scams The Internal Revenue Service is on a constant lookout for tax-related scams. In most cases, “phishing” scams are bogus phone calls and emails that claim to come from the IRS. Remember, the IRS will never: 1. Call you without mailing an official notice first. 2. Demand that you immediately pay your taxes over the phone. 3. Take a debit or credit card number over the phone. 4. Threaten to call law enforcement or immigration services to arrest you for failure to pay. This information is not a substitute for individualized tax advice. Please discuss your specific tax issues with a qualified tax professional. Tip adapted from IRS.gov |

| Footnotes and Sources 1. WSJ.com, February 13, 2026 2. Investing.com, February 13, 2026 3. CNBC.com, February 9, 2026 4. CNBC.com, February 10, 2026 5. CNBC.com, February 12, 2026 6. CNBC.com, February 13, 2026 7. CNBC.com, February 10, 2026 8. WSJ.com, February 11, 2026 9. WSJ.com, February 13, 2026 10. IRS.gov, May 29, 2023 11. Everyday Health, August 25, 2025 |

| Dave Fischesser dave@fischfinancial.com 630-346-3302 Fisch Financial http://www.fischfinancial.com/ |